The “rule” of seven years is perhaps the most prominent credit report factoid known by consumers and the general public. It is actually severely misunderstood by almost everyone that thinks they know it.

A common statement I hear is “after seven years you don’t have to pay it anymore.” This hasty generalization is very misleading. The specific law allows for a creditor to report negative account statuses to the credit bureaus for UP to seven years. (7.5 years to be exact, more on that later.) This law only governs how long the information can remain on your credit report. It has nothing to do with the liability you have on the debt. You will always owe it.

The debt never actually expires, there is no “rule” or “law” that forces a debt to expire after a certain period of time. Most creditors and collection agencies simply give up collection efforts after they lose the ability to credit report an account. This is why consumers can sometimes be shocked when they receive a collection notice for a debt that is often 10, 12, or even 20 years old. Guess what? Technically you still owe that money, the collection agency just ran out of any meaningful tools to collect it. After seven years has passed, nobody will ever see it again on your credit report. It’s like it never happened…

Noww that we have cleared that up, let’s talk about the most important part of this seven year rule.

When does the seven year clock start ticking, and when does it stop ticking? The law clearly says the clock starts 180 days after the original delinquency that led the account to be charged-off or sent to collections. This is known as the “terminal delinquency.” Technically, that means the clock starts six (6) months after your very last payment on the account with the original creditor. Since I see credit reports every single day, I can tell you with certainty that even though the accounts can report for 7.5 years from the last payment you made, credit bureaus today are only reporting for exactly seven (7) years. Not 7.5, even though technically they can. Read the exact text in the FCRA here.

Here is how the seven year rule can apply to items on your credit reports:

Judgments – Seven years from the filing date whether satisfied or not.

Collections – Seven years from date of default with the ORIGINAL creditor, not seven years from when the collection agency buys or is consigned the debt.

Charge Offs – Seven years from the date of the original terminal delinquency.

Settlements – Seven years from the date of the original terminal delinquency

Repossessions and Foreclosures – Seven years from the date of the original terminal delinquency.

Late Payments – Seven years from the date of occurrence.

Can making a payment, or paying a collection reset the seven year statute?

A lot of consumers I speak with are afraid to pay off a collection or even speak to the collection agency because they fear doing so will re-age an old debt and reset the seven years. This is absolutely false, nothing you do can reset the seven years. Paying it won’t, calling them won’t, disputing it won’t. (A partial payment can reset the four year statue for filing a civil suit against you, but that’s a whole different topic we’ll cover in a future blog. )

Just because the FCRA and the law say that’s how long the items can credit report for, doesn’t mean things won’t report for longer. Credit bureaus are handling millions of files and mistakes definitely happen. Collection agencies can also “re-age” the debt (illegally) causing the reporting period to reset. It’s up to you to know your dates and hold the credit bureaus accountable to the reporting statute of limitations, AKA the seven year rule!

Turning 18 is a milestone for most teenagers, and mine was no exception. I was finally legally able to engage in activities teenagers salivate for, such as getting my own apartment, opening my own bank account, obtaining a credit card, and most importantly, trading in my vehicle for something a bit more desirable.

I went to a car dealership to check out some cars, and was quickly approached by a car salesman.

“Mr. Moreno, we will have to check your credit score to determine the terms of your financing,” I recall being told.

What? I had no idea what he was talking about, so I played along. I gave my personal information and waited anxiously while he went to his manager. I curiously watched as they stared at a computer screen and their eyes glinted with satisfaction.

“Congratulations, you’re approved! You have three paid off car loans with your credit union and your credit score is 800!”

I just turned 18. How could this even be possible? Did somebody steal my identity?

This scenario is an absolutely true story, and a growing problem within the consumer credit and finance industry. The technical explanation is the fact that I am a junior, with the same mailing address and name as my father. Fortunately for me, my father valued his credit profile and paid all his bills on time, and due to the similar identities, our credit profiles were merged together. Clearly, we have different Social Security numbers and dates of birth, so what happened?

The three major credit bureaus, Experian, Transunion and Equifax, sell and maintain personal information. They manage and move millions of files on a daily basis, and they often make mistakes. Father and son credit profiles can become one single profile. If you have a common name, your information can be on someone else’s credit profile with a similar identity, and vice versa.

When a consumer examines a credit report, and identifies something that does not belong there, Identity theft is blamed. However, if you look closely at the trade line, it is paid on time, as agreed. What crook is going to steal something and then pay for it? That’s the first sign of a mixed file. Previous addresses reporting on your credit report in places you have never lived? Another indicator.

While an 18 year old can start off with a synthetic 800 credit score, they can also start off with a 500 credit score if their credit twin just happened to have bad payment habits. It’s a serious, growing trend that we have seen locally. Seven out of 10 consumers who come to my office seeking identity theft advice are experiencing mixed credit file problems.

Fortunately, it is far quicker, and easier, to remedy a mixed credit file than it is to battle real identity theft. A simple correspondence to the credit bureaus requesting that they verify all key personal information including Social Security number, date of birth, and true legal name with the information the creditor has on file generally resolves the situation. There may not be a need for police reports, notarized fraud affidavits, or dealing with fraud investigators.

Check your credit report thoroughly, and often. The only free resource to obtain your credit reports is www.annualcreditreport.com; do not be fooled by imitators.

I asked the salesman if he had realized that I could not possibly have paid off car loans when I was 14. I knew something was not right. So I left, and began my journey to obtain my own 800 credit score.

— Anselmo Moreno is a credit consultant with Innovative Credit Solutions, a credit service organization registered with the California Department of Justice. Contact him at amoreno@icscreditfix.com. These are his opinions, not necessarily those of The Californian.

Credit problems? Take action now, because your bad credit is not going to fix itself.

If you are an adult living in the United States, it is a pretty sure bet you have a credit report. It’s also a sure bet that you didn’t learn anything about credit reports and personal finance in school. Now, as an adult, you come face to face with your credit report – basically your adult report card. Are you happy with your grades? AKA your credit scores…

I have been a professional credit consultant for the last 12 years. I have seen consumers from all walks of life have bad credit. The reasons are plenty! A sudden job loss, divorce, bankruptcy, Identity theft, medical catastrophe or just plain old poor money management and overspending. Bad credit can be crippling to your overall financial success.

The one thing everybody who’s ever had bad credit has in common is: It’s not going to fix itself. Some of those consumers choose to ignore their bad credit and live the “I pay cash for everything” lifestyle. But let’s face it, they are not paying cash for their house or new car.

Other consumers choose to take action and become informed about how to credit really works. They research whether or not credit repair can be a good fit for them. As they master their credit score, they are welcomed into the 700 club. (A secret club composed of consumers with a 700+ credit score) 😉

When an eager consumer doesn’t qualify for the financing they require, they often are advised to seek a qualified “co-signer” to allow them to obtain the loan or credit extension. Financially, it’s like juggling knives with your eyes closed.

Four things you NEED to know:

Lenders will count this Debt as Yours – this will count against your debt to income ratio as if you were making the payment.

You are not acting as a reference.

You are just as responsible for the repayment of the debt. Translation: if they don’t pay, you will pay it. All of it, not just “your half.”

It will lead to derogatory reporting if its goes unpaid or paid late, and the credit score impact will be just like if you paid late or failed to pay.

Remember: It is a contract you are signing. You are promising that if anything goes wrong; you will pay the balance, plus interest and penalty fees.

If you already are a co-signer, you need to set some safeguards to protect your credit.

Make sure the statement goes to your mailing address

Ensure the finance company knows how to reach you in case anything goes wrong.

Pay the bill yourself, and have your co-signer pay you.

I cannot stress how important it is to pay the bill yourself to protect your good credit. There is a reason why they need a co-signer, and it is because they do not have a good track record of paying their bills on time.

The bank is already telling you that they do not trust that person enough to lend them the money without your guarantee.

I have seen it end friendships, relationships, and make family gatherings extra awkward.

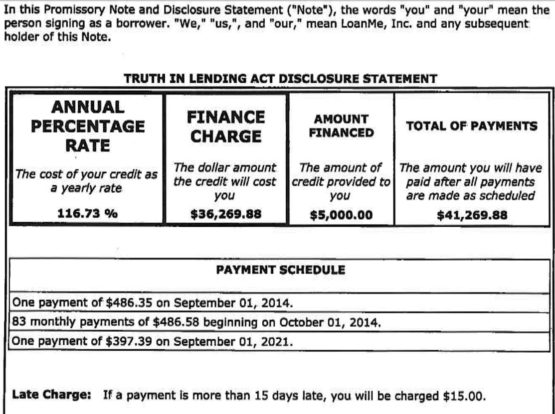

116.73% — Yikes! Today I had a consumer seek out advice regarding a recent court summons he received from an online lender that he borrowed $5,000 from. It was a fairly standard civil complaint for monies, until I saw the Truth In Lending Act Disclosure Statement. Check it out for yourself!

Is this the modern-day Mafia? At the end of the term the consumer would have paid back $41,269.88. Who in their right mind would take out this kind of loan?

That’s exactly the problem. Payday loans, title loans, online loans all are extremely predatory in nature and rely on a consumer who is in a serious financial bind in order to get them to accept these heinous terms. They are not in their right mind and will justify this quick money loan as a means to bridge their financial need immediately. Who’s thinking long-term when your fridge is broken? Your loved one just died? It’s predatory. Having bad credit leaves you with no choice but to deal with these types of lenders. Don’t live with bad credit. The cost of bad credit can be extreme…

Consider this: If you have great credit, you can easily borrow $5,000 at no interest or extremely low-interest. You can repay the loan quickly and not be on the hook for $41,269.88…one of the many benefits of having great credit. I help consumers take control of their credit reports and credit scores.

Have you ever been to the doctor or the emergency room and thought your insurance took care of the bill only to find out later through your credit report that it didn’t? In that case, the changes would directly benefit you.

On August 7th , 2014, FICO, the company behind the most commonly used credit scoring system, announced a new generation of its credit scoring formula with some remarkable changes to the way it assesses consumer credit risk. The new scoring system, known as FICO® Score 9, is designed to bypass the presence of paid collections.

Previous FICO score systems significantly lowered a consumer’s credit score if it detected any collection account on the credit report, paid or unpaid. In addition, the new scoring system also treats unpaid medical collections differently. FICO® Score 9 does not penalize a consumer as much for an unpaid medical collection as it normally does for other unpaid non-medical collections.

Since developing the first FICO credit bureau risk score in 1981, FICO has made several revisions to its credit score formulas that bring the system more in line with current trending consumer spending and payment habits. Thirty years ago, consumers didn’t use debit cards, nor was it a common practice to have rent-to-own furniture or access to credit at every single store in the mall. It is easy to see why updating your scoring system is necessary if you are in the credit risk management business. Read More ▸